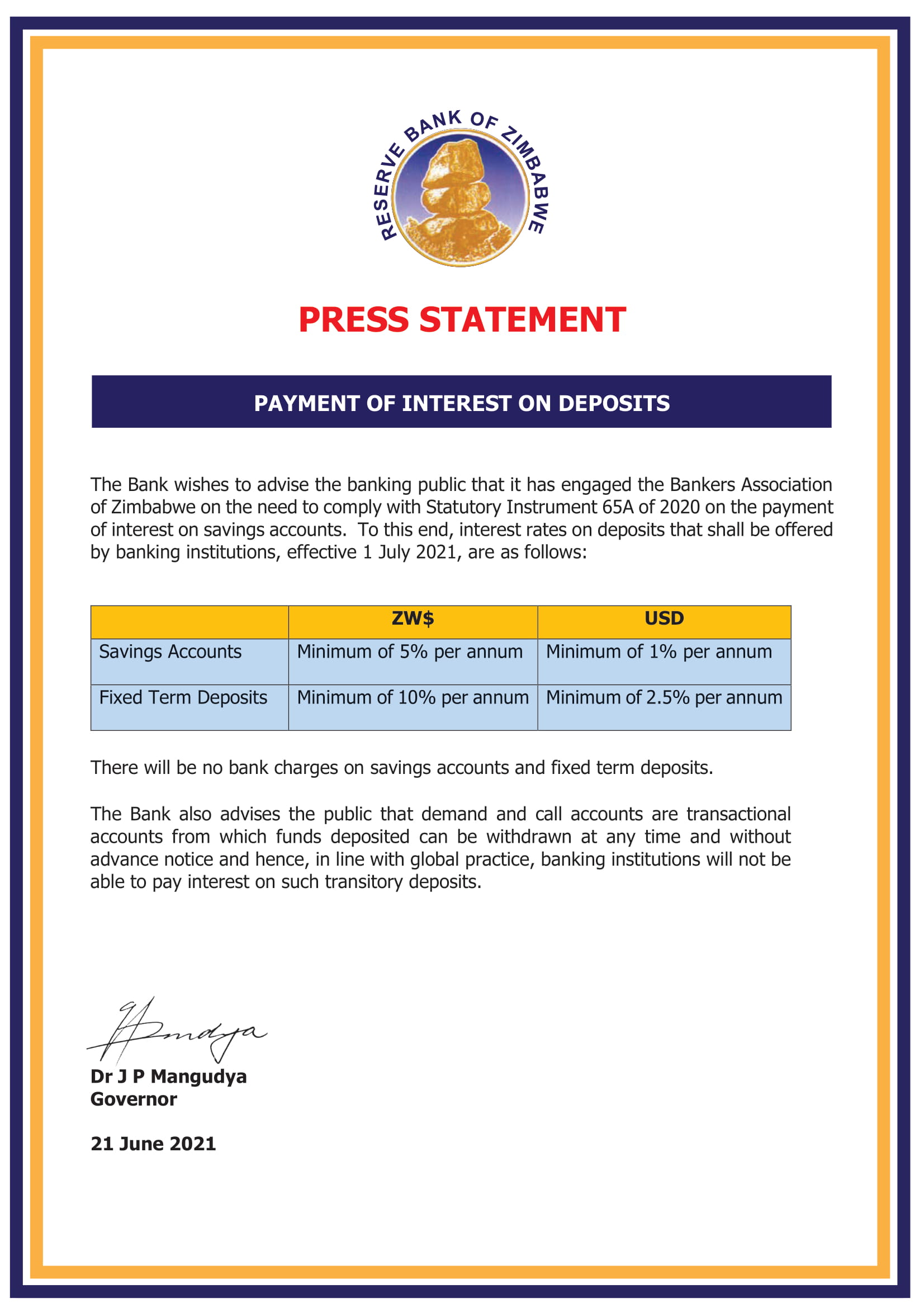

Zimbabwe banks will start paying interest on savings accounts with effect from 1 July, the Reserve Bank of Zimbabwe said in a statement today.

Zimbabwe banks will start paying interest on savings accounts with effect from 1 July, the Reserve Bank of Zimbabwe said in a statement today.

It said interest will be paid on savings accounts and fixed term deposits only but not on demand or call accounts.

There will be no bank charges on savings and fixed term deposits.

Zimbabweans, including Members of Parliament, have complained about the high bank charges on the demand and call accounts saying banks should make their money from lending and not from transactions by the public.

Below is a Q&A on bank charges in Parliament recently:

HON. CHIKWAMA: Thank you Mr. Speaker Sir. My question is directed to the Minister of Finance. Minister, is there any mechanism or plan which makes banks reduce their bank charges which are highly charged especially on payments, transactions or transfer, be it ZIPIT or RTGs?

THE DEPUTY MINISTER OF FINANCE AND ECONOMIC DEVELOPMENT (HON. CHIDUWA): I would like to accept what has been submitted by Hon. Chikwama that bank charges on transactions that are being levied by our banks are on the upper side. We have engaged our banks and the primary reason they are fighting for high bank charges is because of the software system they are using. Most of the systems they are using are imported. We need to continue revamping our availability of forex so that we reduce the costs of imported software. We are also saying they should look at having those solutions locally.

In terms of the short term management of costs, we may not be having the solution on that but in the medium to long term, we are looking at the availing of forex to the bank and also trying to get the local solution.

HON. GONESE: My supplementary question relates to the issue of the banks apparently trying to make money from bank charges. My understanding of banking is that banks must make their profits from lending. In other words, they borrow money or get deposits at lower rates of interest and then lend money to borrowers who then pay higher levels of interest. What is Government doing to ensure that the essence and principle of banking where banks are supposed to make money through lending and not through the lending of bank charges can be rectified thereby lessening the burden on people who have deposited their money having to bear the brunt and sustain the operations of banks?

HON. CHIDUWA: In terms of the operations of banks, commercial banks and all institutions that are allowed to lend are free to provide lending facilities, but it is up to the individual bank to look at the risk profiles of those who are applying for loans. We are not limiting. What only limits the bank is the risk profile but the other issue that is also affecting banks is the unavailability of funds to do the lending programmes. We should also take into account the issue of functions that have affected our banks in terms of the extent to which they can get international credit lines that they can give out to those who are looking for land. Banks are free to provide loans but they also consider the risk profiles of those who are looking for loans.

HON. NDUNA: I am concerned that some of these banks are international banks and they are also resident, some of them in South Africa for example NEDBANK, Stanbic and Standard Chartered where Zimbabwe is also an international bank. If they can charge pittance in terms of charges outside Zimbabwe and using the same system, why is it usurias in Zimbabwe? How much time are you giving them to install software that is affordable on the side of the customers?

HON. CHIDUWA: I still come back to the same point of the soundness of the financial system that we look at the profile of non- performing loans. If you look at the proportion of non-performing loans versus the loan profile, this is what determines the risk profile. As long as our non-performing loans are on the upper side, it then determines the risk profile. In terms of when we are likely to have local solution, I think I would need to engage the Bankers Association of Zimbabwe and then come with a Ministerial Statement.

(154 VIEWS)