On Monday, Reserve Bank of Zimbabwe governor John Mangudya appeared before Parliament’s Public Accounts Committee, where he testified that his strategy to assume over $1 billion in bad bank loans had saved the economy from collapse.

On Monday, Reserve Bank of Zimbabwe governor John Mangudya appeared before Parliament’s Public Accounts Committee, where he testified that his strategy to assume over $1 billion in bad bank loans had saved the economy from collapse.

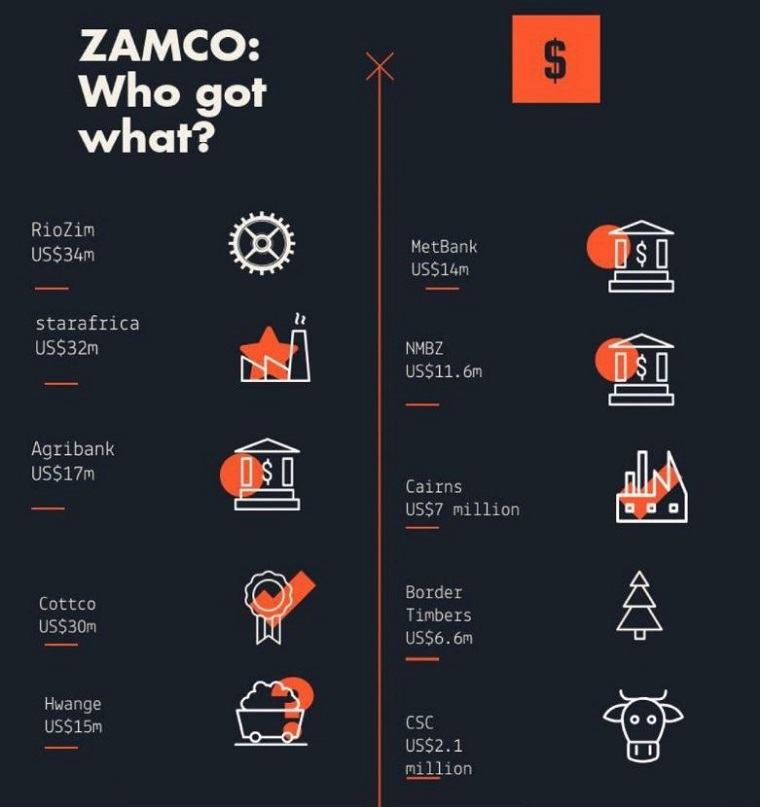

In 2014, the RBZ set up the Zimbabwe Asset Management Company (ZAMCO), to take over bad debts in the banking sector. The ratio of bad loans to total loans had risen to over 20%, above the international standard that such loans be kept below 5%, so as to keep banks safe.

By 2018, ZAMCO had taken up $1.13 billion in bad loans.

In 2018, Finance Minister Mthuli Ncube said he was putting a stop to ZAMCO, as part of his strategy to reduce the budget deficit.

But how and why did we get here? The story of ZAMCO is a mix of success stories in the revival of distressed firms, and also a great deal of top level greed and secrecy.

First, it is important to go back to 2009 to understand what gave rise to ZAMCO.

There are many reasons why people defaulted after dollarization. When the economy moved to US dollars, many people had an inflated sense of how much assets were really worth. This included banks. Some of the assets that borrowers put up for collateral were overvalued.

And when liquidity problems worsened, and many defaulted hit by unforgiving interest rates of as high as 20%, banks were not able to recover their money in full.

Banks either had poor Know-Your-Customer regulations, or overrated some of their ‘high net worth’ clients that had been wealthy in the Zimdollar era. Banks just did not adjust their lending practices from the Zimdollar era to a new US dollar economy.

There was no working Credit Reference Bureau, so it was impossible for banks to find out the truth about their clients; some were over-borrowed and owed many other banks and retailers. Some borrowed and took the money out of the country, with no intention of ever paying back the money.

There was a rush by some companies to borrow for expansion; for example, in just a year between 2010 and 2011, total loans rose from US$1.7 billion to US$2.9 billion. To put this in focus, while the bank loans grew by 70%, deposits only rose by 27%. Something had to give.

Should the list of ZAMCO defaulters be released, as demanded by MPs, we are going to see the names of executives that borrowed from themselves and lent money to their friends. Due to weak oversight, the pile of insider loans increased. In fact, at one bank, more than 90% of the bad loans were insider loans.

A combination of poor supervision, greed, interest rates and liquidity shortages drove up the number of people defaulting on their bank loans. As a result, non-performing loans soared. From 1.62% in 2009, NPLs rose to 3.2% in 2010, 6.17% in 2011, 12.2% in 2012 and 14.51% in 2013.

The figure then peaked at 20.45% in 2014, the year the RBZ then decided to do something drastic about it.

Continued next page

(450 VIEWS)