Government has gazetted the Zisco Debt Assumption Bill, effectively taking over the steel giant’s debt, clearing the way for its takeover by Chinese firm, Tian Li and its revival.

According to the bill gazetted yesterdayy ZISCO’s debt stood $494 million as at December 2016 with $211.9 million of that being external loans owed to KFW (Germany), Sinosure (China) and Sumitumo (Japan) who are owed a total of $6 million.

Domestic loans amount to $56 million while domestic suppliers, utilities and statutory obligations are at $219 million.

The ZISCOsteel board is set to convene an Extraordinary General Meeting next Thursday to seek approval from minority shareholders for Hong Kong based firm Tian Li to takeover the steel maker.

Tian Li is a subsidiary of R&F Properties which last August agreed to invest up to $2 billion in Ziscosteel.

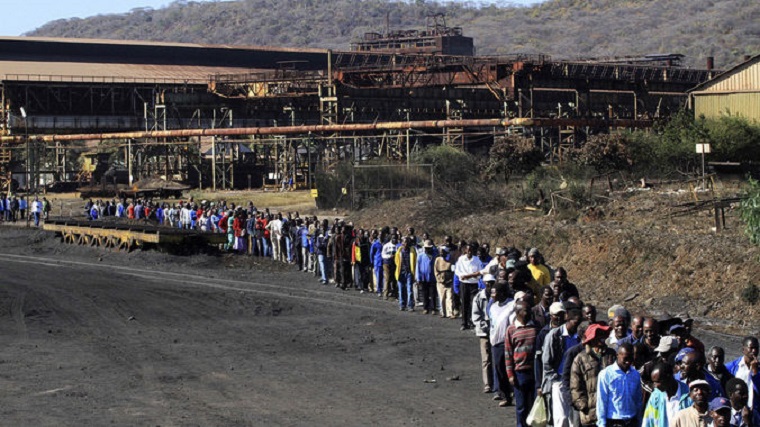

The restart of Ziscosteel, which was the biggest integrated steel manufacturer in Africa before its collapse in 2008, is seen as key to reviving Zimbabwe’s economy.

Its resuscitation would also be crucial to the operations of Hwange Colliery Mine and the National Railways of Zimbabwe (NRZ), which are both struggling but are targeted for revival.- The Source

(196 VIEWS)

This post was last modified on January 31, 2018 4:55 am

Zimbabwe has been ranked third among the least free countries in Southern Africa but it…

I had always considered it a curse for a wife to die before her husband.…

This is a true story about the challenges and loneliness I faced when my wife…

My first long-form article in booklet form: Why I had a girlfriend two months after…

The editor and publisher of The Insider, Charles Rukuni, has started a whatsapp channel through…

A friend who knows about my legal battle with Zimbabwe’s richest man, Strive Masiyiwa, way…

{kind=link}